Mumbai, March 21, 2025: Emkay Investment Banking – the investment banking arm of Emkay Global Financial Services Limited held a virtual media webinar on the state of affairs of the Indian investment banking industry, key highlights and the outlook for the IB industry. While the correction in the market has slowed down activities in the deal street, the government divestment plan is likely to provide a push to the fund raising activities. The SIP flows and DII buying has negated the FII outflows.

Fund raising by PSUs at centre stage

Public sector is turning out to be a material client for Investment Banks in India. The Department of Investment and Public Asset Management (DIPAM) has set a divestment target of Rs 47,000 crore for FY26. This is a huge opportunity for Investment Banks in FY26 and beyond. In the past 3 years, IPOs of LIC, IREDA and OFS of ONGC, IRCTC, HAL, Coal India, RVNL, NHPC, Hudco, Ircon, Cochin Shipyard has kept the deal street buzzing from the PSU segment. The ongoing IPOs of Bharat Coking coal, CMPDI, MNGL and QIP/OFS of IREDA, GRSE, Veedol, Central Bank, Uco Bank, IOB, Bank of Maha, Punjab & Sind is likely to provide prospects to the investment banking industry in FY26 and beyond.

Correction in secondary market is reflecting on the primary markets

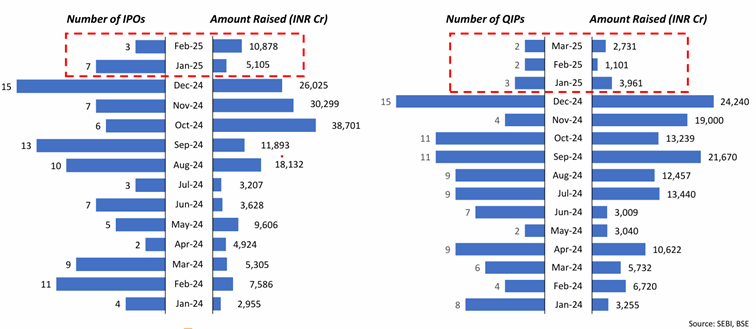

The correction in the equity market has started showing its impact on fund raising activities. CY24 saw 92 IPOs, thereby raising over Rs 1,62,261 crores, whereas companies raised over Rs 1,36,424 crores via 91 QIPs. If we compare the YoY data, the IPOs in Jan-Feb 2025 is limited to only 10 vs 15 in Jan-Feb 2024, whereas QIPs in Jan-Mar 2025 is limited to only 7 vs 18 in Jan-Mar 2024.

SIP flows to the rescue

The resilient SIP inflows are supporting markets to a large extent. SIP flows has been over Rs 20,000 crore for the past 11 months (entire FY25, April 2024 till February 2025). The SIP flows has risen to over Rs 25,000 crore for the past 5 months which is quite an encouraging sign, this despite negative returns from the market since September 2024. The street was expecting a slowdown, fall in SIP flows, – which is quite normal in a falling market. A fall in SIP going forward could have a severe impact on overall market performance.

DII inflows negating FII outflows

DII inflows has more than compensated for the FII outflows in FY25. As per the available data, DIIs have invested over Rs 5,70,000 crore in the market vs 2,88,000 crore in the 11 months of FY25.

RBI rate decision, liquidity measures key to market performance

Key decisions by the RBI to boost lending is expected to trigger liquidity in the markets in the near to medium term. The bank credit is expected to get a strong boost in the medium to long term due to

- Repo rate cut

- Relaxation of risk weights for SCBs on NBFC loans by 25%

- Liquidity measures undertaken by the RBI

- Measures announced in the Union Budget to boost consumption demand